This post is sponsored by the Alliance for Lifetime Income, an Official Personal Finance Partner of Growing Bolder.

This post is sponsored by the Alliance for Lifetime Income, an Official Personal Finance Partner of Growing Bolder.

The coronavirus economy has shaken millions of Americans’ confidence in their ability to retire comfortably. In fact, 70% of Americans say the pandemic has made them more pessimistic about their retirement plans, according to a recent Retirement Reset survey. Another survey shows almost half of all parents have given their adult children money during the pandemic, with most saying they’re doing so at the expense of their own personal finances.

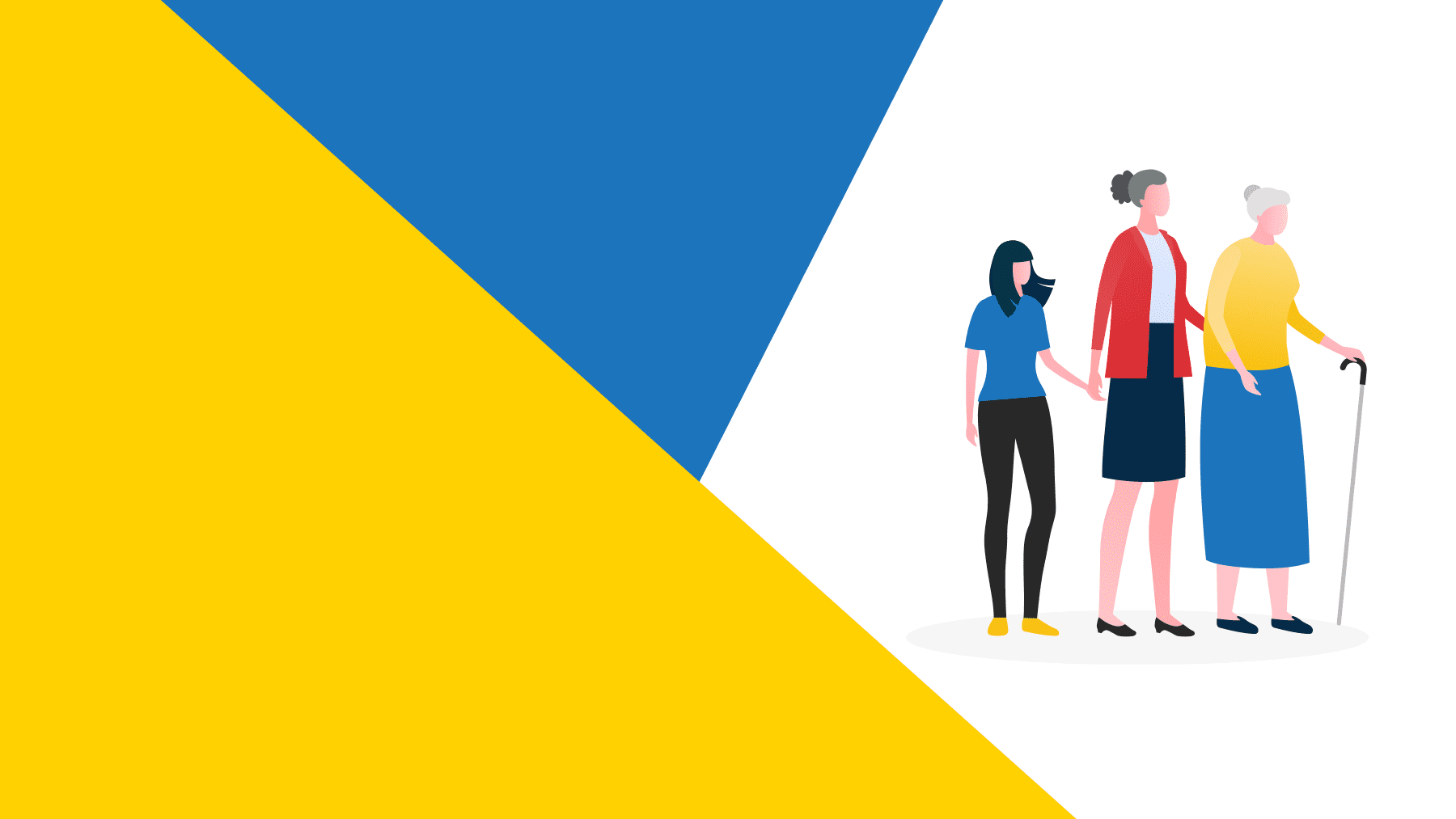

Older Gen Xers and younger Boomers in particular have been forced to reconsider or restructure their retirement plans in the pandemic’s wake to account for unexpected obstacles. Namely, adult children who have moved back home by choice or due to lost income, and aging parents who require financial assistance to afford long-term care or their own retirement.

Left to juggle the costly and often time-consuming needs of both dependents, demographers often refer to this select group as the “sandwich generation.” Stretched thin, these multigenerational caregivers—typically parents in their prime working years—are subject to a unique set of challenges that have been further exacerbated, thanks to the pandemic.

Twelve percent of Americans currently fall into this group, according to data from the Pew Research Center. However, this number is expected to rise, as more individuals prepare for retirement and more millennial families delay having children.

If you’re among this group of Americans feeling overwhelmed, there are several things you can you do to help ease that stress, including:

Assess your finances: Before you sit down to figure out what kind of assistance you can provide to your loved ones, make sure you have a complete picture of your own finances. Establishing boundaries between what you want to do and what you’re financially able to do is important and will help you avoid any surprises or disappointment in the future.

Plan ahead: To help minimize stress and anxiety, establish a healthy financial plan, with clear goals to help ensure you don’t outlive your resources. And when it comes to having the income you need in retirement, protected income from an annuity is a great way to guarantee income for life and combat the risk of running out of money. It can help supplement the other source of protected income, like Social Security, and can be especially valuable if you don’t have a pension.

Talk with your parents about money early and often: Have a candid conversation with your parents about their financial situation and what their needs are before a crisis hits. Make sure you fully understand what funds they have, where they are located, and any penalties associated with early withdrawals.

Involve your children in financial conversations: While you’re talking over expectations with your parents, take time to do the same with your kids. Maintaining open communication with your children, especially when times are difficult, is an opportunity for you to impart important financial education and values, priorities and behaviors that will help them make good financial decisions when they are older.